Why are my FD rates going down?

Investing

|

May 28, 2020

Fixed Deposits are one of the most preferred products for investors looking for safety of returns. However, in recent times the interest rates one earned from their fixed deposits has consistently been reducing. While the existing depositors have not been impacted, those looking to make fresh deposits are surely concerned.

So how has COVID played a part in not just wreaking havoc in our mobility, but also our financial lives?

Let’s break it into two parts

What is happening in the economy

What is happening at the bank

What’s happening in the economy?

With the country getting into pause mode, several businesses have faced a loss of earnings, and several people have lost their jobs, i.e. income loss. Loss of revenues, reduced incomes or no incomes – all this amounts to an expected ‘recession’.

A recession means a circular loop of less money to spend and hence lesser earnings for businesses. Imagine this situation as a gradual slowing down of water flow from a tap. Now to make sure that the water doesn’t stop completely, the central banks take certain SOS measures. Akin to switching on the pump to restart the water flow, they find ways to increase the money in people’s hands which would help them buy more, and hence grow businesses to earn more.

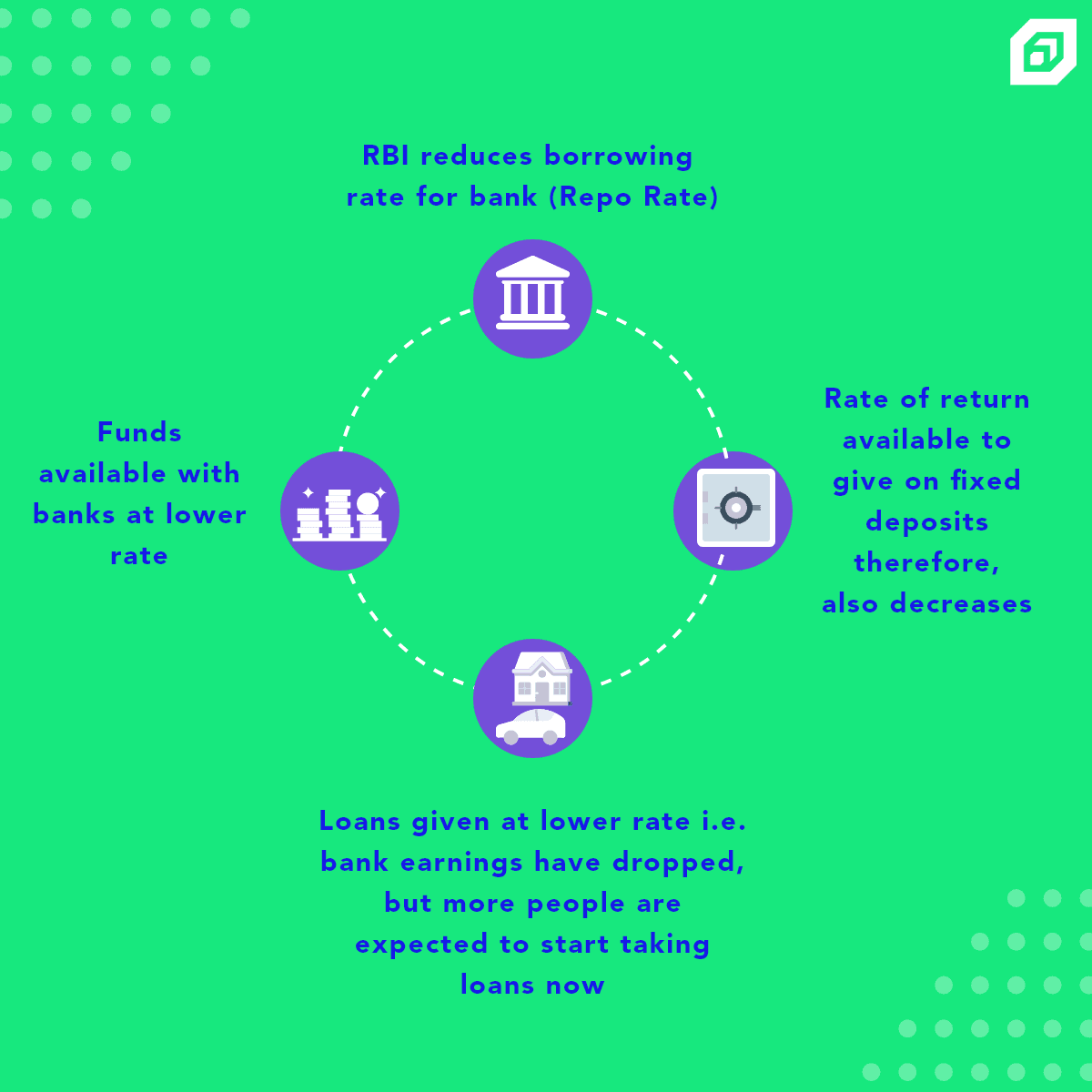

Few of these measures include a ****change in the Repo Rate – the rate at which banks borrow from the central bank (RBI in our case). Reduction in the Repo Rate means banks can borrow funds cheaper and therefore, provide the same at lower rates to those who need funds.

Since June 2019, the central bank has cut the repo rate seven times, with the hope to re-fuel the growth in the economy. As per the latest rate cut, it stands at 4 per cent compared to 6.5 per cent in February 2019.

What’s happening at the banks?

With cheaper availability of funds, banks are now passing this benefit as lower-cost loans – home loans, car loans and so on.

This means the bank’s earnings from loans, i.e. the interest, has decreased.

Since the bank’s earning has decreased, it possibly cannot provide its depositors with a high return on their FDs.

Hence large banks, including the State Bank of India have reduced their FD rates to sub-6per per cent levels (5.5 per cent for one year FD and 6 per cent for senior citizens) for the first time since 2004.

Here is how the flow of money looks :

Options if I still want to invest in FDs?

Reports suggest that it is likely that FD rates will reduce even further. But, if you still prefer the safety of fixed deposits here is what you can do.

If you are an existing FD investor, hold onto your deposits. If you are a fresh investor and keen on FDs you could consider 5-year tax-saving FD investments which give an additional tax benefit.

In case you have a longer horizon for the available funds, consider the Government small savings schemes. Such as post-office 5-year time deposits (6.7 per cent), National Savings Certificates (6.8 per cent annual interest) with a lock-in of 5 years, which offer better interest rates compared to fixed deposits.

For senior citizens looking for more avenues, senior citizens’ savings scheme with a 5-year lock is another option, which provides quarterly interest.

Read More

Unleashing Alexis Rose's PR Magic: Building Her Own Empire

May 28, 2020

Unlocking your go to guide to navigate Gold 🌟

May 28, 2020

Investing in Gold 101 - A handbook on why, and how to invest in Gold

May 28, 2020

Is Taylor Swift REALLY saving the US Economy?

May 28, 2020

6 Lessons from The One-Page Financial Plan by Carl Richards

May 28, 2020

5 Reasons You Need a ̶P̶r̶e̶p̶a̶i̶d̶ Power Card

May 28, 2020